Boeing to Increase 737 MAX Production to 47 Jets per Month After FAA Nod

Dear Readers, Welcome to AviationOutlook.

Let’s analyze today’s topic in detail.

The narrowbody production race has just shifted gears.

Boeing’s chief executive, Kelly Ortberg, confirmed that the planemaker has cleared the regulatory bar to lift its 737 MAX output from 42 to 47 aircraft per month, a milestone that customers, suppliers, and regulators have been watching for nearly two and a half years.

The announcement, made at a Bernstein investor conference, signals that the capstone review for rate 47 has been passed, and the Renton final assembly line is already running at the new cadence as it stabilizes through the summer.

For aviation stakeholders, it’s the clearest signal yet that the post-Alaska Airlines Flight 1282 regulatory regime is moving from a punitive numerical cap to a performance-based oversight framework.

Recommended - Read Full Reports

Read All Reports

A Long Climb Back From the 38-Jet Cap

The story of rate 47 begins in January 2024, when a door plug separated mid-flight from an Alaska Airlines 737 MAX 9 over Portland, Oregon.

The incident, later attributed by the NTSB to four missing retention bolts, triggered an immediate FAA-imposed production cap of 38 jets per month on the MAX program.

That cap stayed firmly in place through 2024 and most of 2025, while Boeing rebuilt its quality management apparatus, retrained mechanics, and absorbed the financial drag of slower output.

KEY MILESTONES IN THE 737 MAX PRODUCTION RAMP

• Jan 2024 — Alaska Airlines Flight 1282 incident; FAA caps MAX output at 38/month

• Oct 2025 — FAA lifts hard cap; Boeing authorized to step up to 42/month

• Mar 2026 — FAA replaces hard cap with performance-based oversight model

• May 27, 2026 — Ortberg confirms capstone review for rate 47 passed

• Summer 2026 — Rate 47 stabilization expected at Renton FAL

The FAA’s initial loosening came in October 2025, when it allowed Boeing to increase output to 42 aircraft per month. That figure held as an interim ceiling while the agency monitored Boeing’s quality data closely.

By early 2026, the FAA had begun shifting back some airworthiness ticketing authority to Boeing’s authorized representatives, a quiet but consequential signal that the regulator trusted the planemaker’s internal controls again.

What “Rate 47” Actually Means Inside Renton

At the Bernstein conference, Ortberg said the company has “passed the capstone review for rate 47” and is “in the process of running the line at the 47-a-month rate,” with the caveat that it will take “a few months of stabilization.”

In practice, that means jets are now being sequenced onto the moving line at the higher tempo, but takt time, station balancing, and supplier deliveries still need to settle into a sustainable rhythm.

WHY 47 IS THE OPERATIONAL THRESHOLD

• 47 jets/month is roughly 564 aircraft/year, close to pre-MAX-grounding cadence

• It allows the program to begin meaningful backlog reduction

• It tests whether the new "performance-based" oversight model holds under stress

• It is the gateway to the next published target of 53/month by year-end 2026

Inside the factory, the climb from 42 to 47 looks deceptively small, but it requires every supplier, every quality inspector, and every overtime hour to align.

A single shortage of a high-criticality part can cascade into “traveled work,” which is the unfinished work that moves down the line and then has to be retrofitted later, a metric the FAA now monitors as a leading quality indicator.

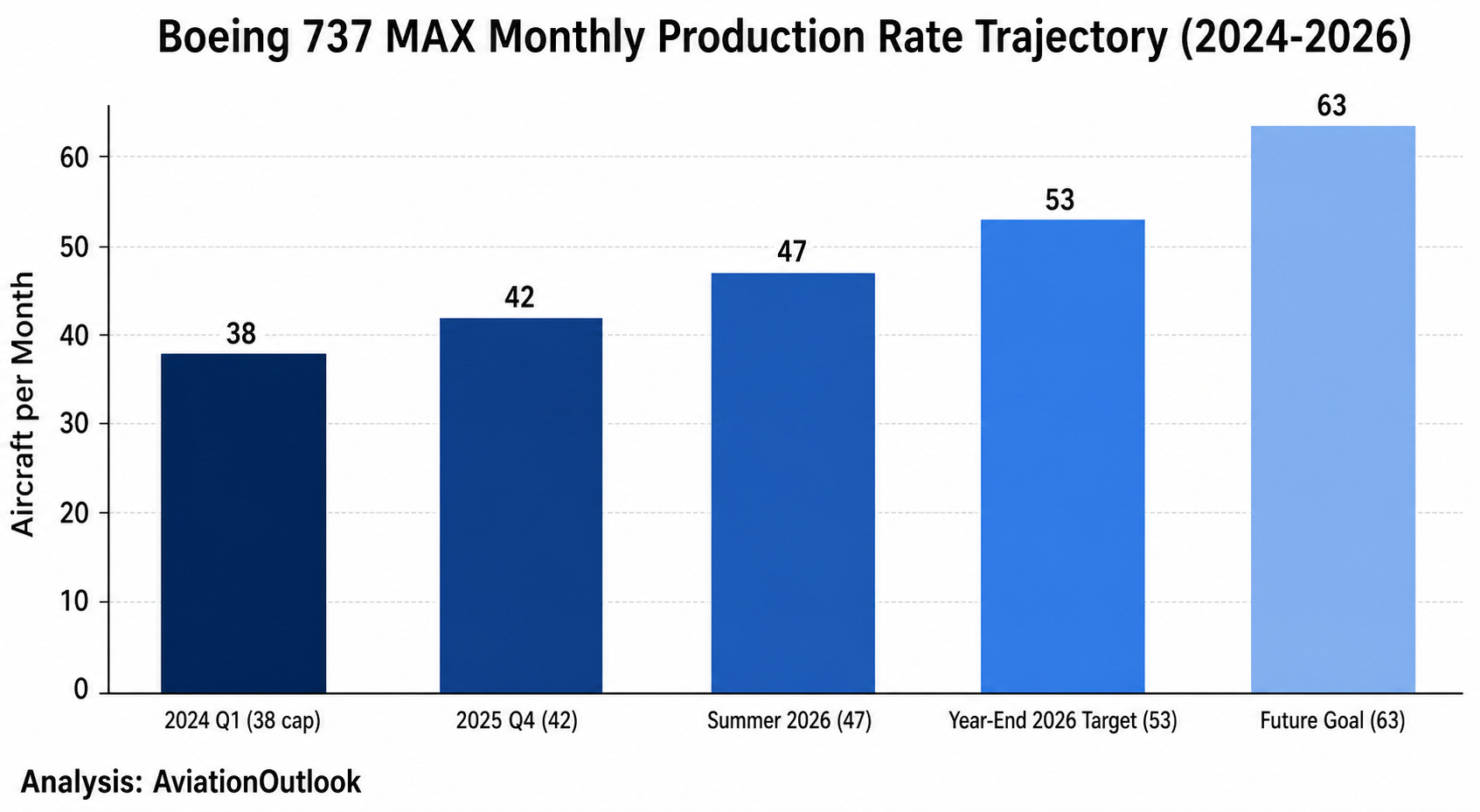

Image source: AviationOutlook analysis. The chart visualizes the staged climb in 737 MAX monthly output, from the 38-jet FAA cap imposed in 2024 to the 47-jet rate cleared in May 2026, the 53-jet target by year-end, and the longer-term aspiration of 63 jets per month.

From Numerical Cap to Performance-Based Oversight

The most significant regulatory change is not the number 47 itself, but the framework behind it.

In March 2026, the FAA formally replaced its hard numerical ceiling with an oversight model anchored in Safety Management System maturity and live production data.

That shift means future rate increases are gated by metrics, not by political optics or arbitrary thresholds.

The two metrics that now matter most are “traveled work” and “quality escapes,” the latter referring to defects that slip past internal inspection points.

If both stay within agreed bands, Boeing is authorized to keep stepping up output without seeking a fresh waiver each time.

THE NEW OVERSIGHT MODEL IN ONE GLANCE

• Anchor: Safety Management System maturity (SMS Maturity)

• Inputs: Traveled work, quality escapes, defect rates, audit findings

• Outputs: Delegated ticketing authority returns to Boeing reps

• Trigger: Sustained green-zone metrics unlock the next rate step

• Risk control: FAA retains right to throttle production if metrics slip

For airline stakeholders, this changes the planning calculus.

Delivery schedules no longer hinge on a binary “cap raised or not” decision in Washington.

Instead, they hinge on whether Boeing can keep its factory-floor data clean, which is a more granular and more predictable variable to model.

For Boeing’s own leadership, the framework rewards discipline and punishes shortcuts in close to real time. The carrot is more aircraft out the door, the stick is an immediate freeze if defect data deteriorates.

The Spirit AeroSystems Factor

In December 2025, Boeing completed its acquisition of Spirit AeroSystems, the Wichita-based supplier that builds 737 fuselages, ending more than two decades of outsourced fuselage manufacturing.

That reintegration gave Boeing direct, “nose-to-tail” control over fuselage quality, the same component family that triggered the door plug failure.

The deal also folded roughly 15,000 Spirit employees and their Boeing-related work into Boeing’s commercial airplanes unit, including major structures for the 787 program.

For the MAX line, the practical effect is that fuselage defects can now be addressed under a single quality system rather than negotiated across a supplier interface.

That matters because supplier handoffs are historically where “traveled work” originates, and traveled work is precisely the metric the FAA is watching.

WHY THE SPIRIT DEAL MATTERS FOR RATE 47

• Single quality management system across fuselage and final assembly

• Direct accountability for upstream defects, no contractual back-and-forth

• Faster engineering change incorporation on the production floor

• Tighter alignment between supplier hiring cadence and FAL takt time

• Reduces the "blame gap" the FAA cited as a root cause in 2024

There are still industrial frictions to manage.

Spirit’s Wichita workforce operates under different labor agreements than Boeing’s Puget Sound machinists, and harmonizing those systems is a multi-year project that runs in parallel with the rate ramp.

Clearing the Shadow Factory and Scaling the Workforce

Two other structural changes deserve attention.

First, Boeing has closed the Moses Lake “shadow factory”, the auxiliary site in central Washington where parked MAX aircraft from the 2019 grounding era were being reworked and reinspected.

Clearing that backlog released more than 1,000 specialized mechanics back into the active final assembly lines, where they are now contributing directly to new-build output rather than legacy retrofit work.

Second, Boeing is hiring aggressively.

The company is reportedly onboarding more than 100 factory workers each week, an unusual pace for an aerospace original equipment manufacturer.

A fourth production line in Everett, Washington, has also been activated, marking the first time the MAX is being built outside the traditional Renton facility.

That geographic diversification reduces single-site risk and adds physical capacity that becomes essential as the program targets “rate 53” by the end of 2026.

WORKFORCE AND FOOTPRINT CHANGES SUPPORTING RATE 47

• 1,000+ mechanics redeployed from Moses Lake to active FALs

• 100+ factory hires per week across the MAX program

• New fourth final assembly line stood up in Everett, WA

• Renton remains primary MAX FAL, now running at 47/month cadence

• Cross-training programs expanded to support 7-day operationsThe Backlog Problem That Rate 47 Is Designed to Solve

The strategic urgency behind rate 47 sits in the order book.

Boeing carried roughly 4,763 MAX aircraft in backlog as of March 31, 2026, with lessors alone accounting for nearly 1,300 of those firm orders.

At a steady-state output of 42 jets per month, Boeing would need roughly nine years just to deliver the current order book, assuming zero new orders.

That math is unsustainable for two reasons.

First, airline customers cannot wait a decade for fleet renewal, particularly as they face fuel-efficiency and emissions pressures on older aircraft.

Second, Boeing risks ceding more market share to Airbus on the A320neo family if delivery slots remain scarce.

Rate 47 starts to bend that curve.

At 564 aircraft per year, Boeing finally moves into territory where new orders and deliveries can come into rough balance, with marginal backlog reduction.

Rate 53 is the level at which meaningful backlog burn-down begins. And the longer-term aspiration of 63, which Ortberg explicitly named at the Bernstein conference, would put MAX output back at the peak rates last seen before the 2018 and 2019 accidents.

BACKLOG MATH AT KEY PRODUCTION RATES

• At 42/month: 504 aircraft/year — backlog grows or holds steady

• At 47/month: 564 aircraft/year — near equilibrium with new orders

• At 53/month: 636 aircraft/year — meaningful backlog reduction begins

• At 63/month: 756 aircraft/year — aspirational, historical peak rate

Lingering Risks and the “Whole World Is Watching” Caveat

Ortberg himself flagged the fragility of the moment.

He acknowledged that moving from 47 to 52 will take “at least six months, if not longer,” and that he is not yet confident the company can sustain a 57-per-month rate, which Boeing has hit in earlier eras but cannot replicate today without rebuilding stability margins.

His phrase “the whole world’s watching to make sure we make 47 and 52” was unusually candid for a CEO statement.

There are concrete risks on the horizon. Rail deliveries of fuselages from the former Spirit operations reportedly slowed in March 2026, and a wiring check on certain MAX aircraft modestly disrupted second-quarter deliveries.

In March, Boeing delivered 46 aircraft total, of which 33 were MAX jets, still short of what a true 42-per-month cadence would imply on a sustained basis.

The FAA’s new oversight model is also untested at scale.

If quality data slips during the rate 47 stabilization, the agency has explicitly retained the right to throttle production.

That would be a far more agile intervention than the 2024 hard cap, but it would also be far more disruptive to airline planning, because schedules would adjust in weeks rather than months.

RISK FACTORS TO MONITOR THROUGH H2 2026

• Stability of "traveled work" and "quality escapes" metrics

• Continuity of fuselage rail deliveries from Wichita

• Labor harmonization between Spirit and legacy Boeing workforces

• Engineering change traffic during rate transition

• Any new in-service findings that prompt fleet-wide actionsWhat This Means for Airline Customers and the Wider Industry

For airline planners, the most actionable takeaway is that delivery slot visibility should improve through the second half of 2026. Carriers with firm orders in the early 2027 production positions can now plan with greater confidence on entry-into-service timing, crew training pipelines, and route-network adjustments.

Lessors, who hold roughly one-fifth of the MAX backlog, gain more flexibility to place aircraft with secondary customers as delivery cadence stabilizes.

For maintenance, repair, and overhaul providers, the ramp has a downstream effect. A 12 percent increase in monthly production translates into a proportional increase in induction volumes for engine MRO, line maintenance, and component pool servicing within roughly 18 to 24 months of delivery.

For training organizations, the ramp accelerates demand for type-rated pilots and licensed maintenance engineers on the MAX platform.

INDUSTRY-WIDE IMPLICATIONS OF RATE 47

• Airlines: Better delivery slot visibility, easier fleet planning into 2027

• Lessors: More predictable placement timelines for ordered aircraft

• MRO providers: Ramp in induction volumes from 2028 onward

• Training organizations: Higher demand for MAX type ratings

• Suppliers: Pressure to match 47/month cadence on consumables and rotables

The competitive context with Airbus also tightens.

The A320neo family continues to run at high cadence in Toulouse, Hamburg, Mobile, and Tianjin, and any sustained Boeing recovery narrows the delivery gap that has favored the European planemaker since 2019.

For airlines operating mixed fleets, that competitive parity is generally good news, because it preserves negotiating leverage on price, delivery slot, and customer support packages.

The Road From 47 to 53 and Beyond

Looking at the next 12 months, the program’s critical path runs through three checkpoints.

First, Boeing must stabilize at 47 through the summer without triggering a quality-metric exception.

Second, the company needs to demonstrate that its new Everett line is delivering aircraft at the same quality standard as Renton.

Third, the supplier base, particularly the engine suppliers and the now-internal Spirit operations, must scale in lockstep without introducing rotable shortages.

If those three checkpoints clear, rate 53 by year-end 2026 is plausible.

If any of them slip, the timeline extends, and the FAA’s performance-based oversight will be the visible signal.

Ortberg’s own framing, that the company is “off and rolling” but still has “work to do,” is the most honest summary of where the program stands today.

CRITICAL PATH TO RATE 53 BY DECEMBER 2026

• Stabilize rate 47 at Renton through Q3 2026

• Bring Everett FAL to certified production quality

• Sustain fuselage cadence from internal Spirit operations

• Hold "traveled work" within agreed FAA bands

• Demonstrate clean audit findings across two consecutive quarters

The rate 47 milestone is not the end of Boeing’s recovery arc, but it’s the most concrete operational evidence so far that the company’s safety and quality reset is producing measurable results.

For an industry that has watched the MAX program move from grounding to grounding-adjacent caps for the better part of seven years, the simple fact of a production rate moving up under a stable regulatory framework is, in itself, a meaningful inflection point.